Net Worth Tracker in 2026: Open-Source Spreadsheet Alternative for Multi-Currency Households

I keep seeing the same personal finance spreadsheet: 11 tabs, three currencies, one balance copied by hand, and a bright red cell that says "fix later."

A week later nobody remembers what needed fixing. A month later the totals still look clean. That is the dangerous part.

When a spreadsheet starts lying, it usually lies very politely. Your net worth tracker still has formulas, colors, and a total at the bottom. It just stops being something you would trust enough to make a real decision from.

That is why I think a lot of people do not need another prettier template. They need a better system.

Why a spreadsheet stops working as a net worth tracker

I understand why people start there. A spreadsheet is flexible, cheap, and feels like control. If all you want is a quick monthly snapshot, it is fine for a while.

Then real life shows up:

- salary lands in one account

- savings sit somewhere else

- card balances move during the month

- you transfer money between your own accounts

- one account is in EUR and another is in USD

Now the spreadsheet is not just storing numbers. It is quietly becoming your accounting system, which is where it starts drifting.

A spreadsheet can show a result. It is much worse at preserving the chain of truth that produced it.

What a net worth tracker actually needs

Most people describe net worth tracking as one formula: assets minus liabilities.

That part is almost too simple to matter. What matters is whether the system underneath keeps balances honest over time.

A useful net worth tracker needs four boring things:

- account balances that stay tied to real accounts

- transfers between your own accounts that do not fake income or spending

- transaction history that stays in the original currency

- reporting that can summarize everything in one view when you need it

The formula is easy. The model is the hard part.

Why multi-currency households break weak setups

This is where most spreadsheet systems start lying.

If you live in one country, get paid in one currency, and keep all your money in one bank, you can get away with a lot of shortcuts.

If you are an expat, a freelancer, a remote worker, or just somebody with money spread across countries, those shortcuts stop being cute.

You need a multi-currency net worth tracker, not a nice-looking table with homemade FX logic hidden in random cells.

Here is the trap I keep seeing:

- one sheet per currency

- one summary tab

- manual exchange rate columns

- another column to explain which rate was used

- a note to remember that this transfer was "internal"

At that point the spreadsheet still looks organized. It just stops being dependable.

That is a bad trade. Financial tools do not need to look simple. They need to stay true.

The transfer problem is where trust usually breaks

Moving your own money should be the least interesting event in your system. In weak setups, it becomes the most confusing one.

You move cash from checking to savings and suddenly one side looks like spending, the other side looks like income, and your monthly summary becomes an improv performance.

The same thing happens when people maintain one app for expenses, another sheet for assets, and a third place for notes. The data stops agreeing with itself.

A good spreadsheet alternative does one important thing better: it treats balances, transactions, and transfers as part of one model instead of three separate habits.

That is much less glamorous than another personal finance dashboard.

It is also much more useful.

Why I think open source matters here

Personal finance software gets very opinionated very fast. The moment a tool makes the wrong assumption about currencies, transfers, or reporting, you feel that mistake everywhere.

That is why I like the open-source route for this category.

With an open source budget tracker, the system is inspectable. The data model is not a black box. You can self-host it, read the docs, and understand what the tool is actually doing with your numbers.

That matters even more when you are using the same system for budgeting, balances, and net worth tracking.

Once the data is shared, every bad assumption spreads further.

Net worth tracking works better when balances and budgeting live together

This is the part a lot of people miss. Net worth is not only a number you check once a month to feel responsible. It becomes much more useful when it lives next to the rest of your money workflow.

If the same system already knows:

- what accounts you have

- what their balances are

- which transfers happened between them

- what spending categories are doing

- what the next months are likely to look like

then your net worth view stops being a separate ritual. It becomes part of the same financial picture.

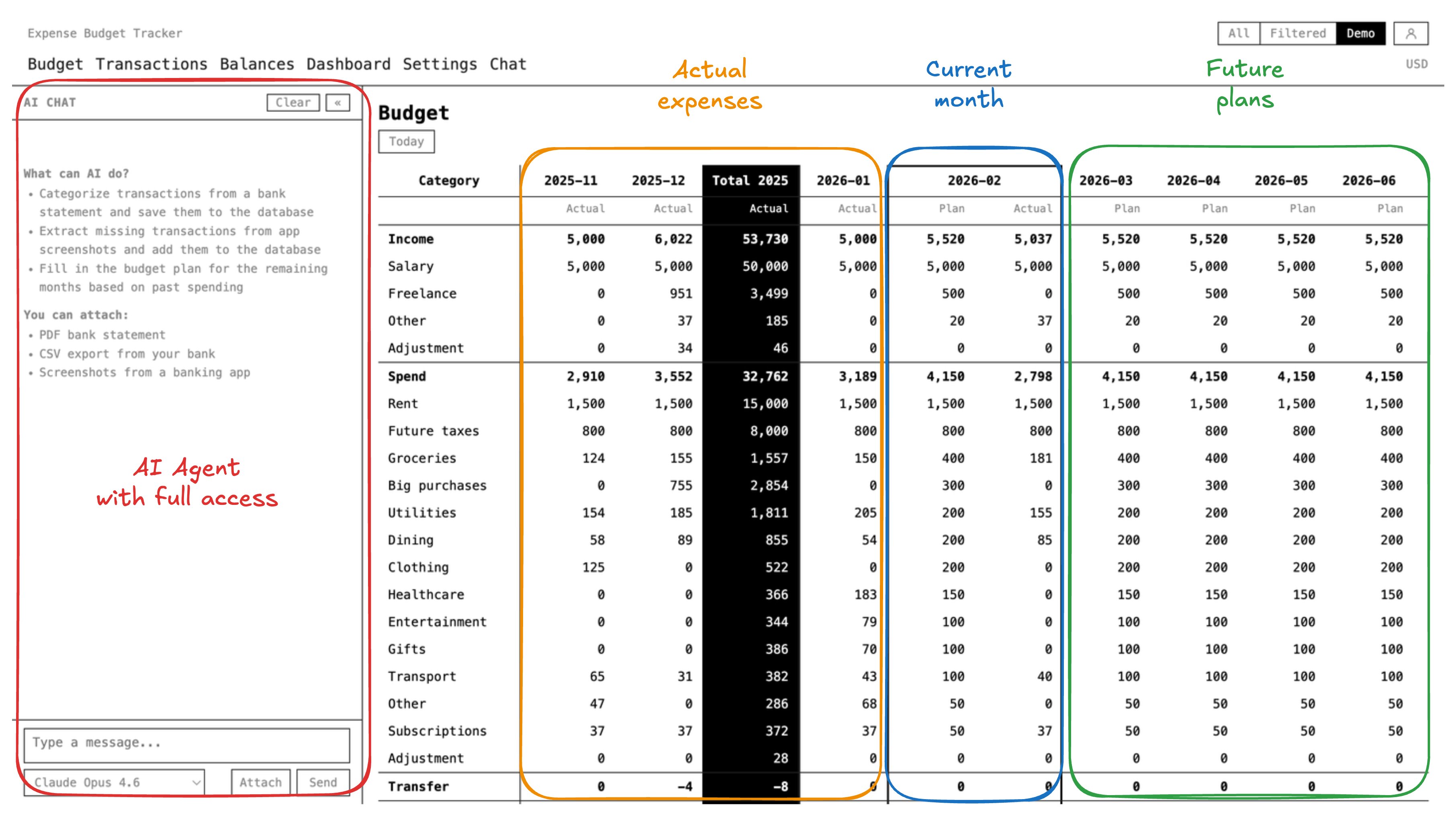

That is one reason Expense Budget Tracker is a better fit for this than another spreadsheet. It already treats balances, transfers, categories, and multi-currency reporting as one system. You are not stitching together a net worth view out of unrelated tools.

Where spreadsheets drift and Expense Budget Tracker does not

The core difference is simple: spreadsheets are flexible by default, but they rely on you to keep the structure honest.

Expense Budget Tracker is stricter in the useful places:

- accounts keep their own native currency

- transactions stay in the currency they happened in

- transfers between your own accounts stay transfers

- reporting converts for analysis instead of rewriting source truth

That sounds like backend detail. It is not.

That is exactly what keeps a net worth tracker trustworthy once you stop living the "one account, one country, one salary" version of life.

Where AI helps with the boring finance work

I do not think AI is the interesting part of personal finance. I think boring admin is the problem, and AI happens to be useful there.

Most people do not give up on tracking net worth because the idea is too hard. They give up because the maintenance is annoying:

- exporting statements

- classifying transactions

- checking balances

- spotting duplicate transfers

- figuring out why one account does not reconcile

That is exactly where AI can lighten the workflow. Expense Budget Tracker exposes a practical agent workflow through its API and SQL surface. That means you can export statements, let the assistant help with categorization and reconciliation, then review the result instead of manually typing everything yourself.

That is the right use of AI here. Not fake advice. Not decorative summaries. Less repetitive admin.

A better way to think about net worth

I would not start with the formula. I would start with one question: do I trust the path from raw account activity to the final number?

If the answer is no, the problem is usually not your discipline. It is the system.

A personal finance spreadsheet alternative is worth using when it reduces manual glue work, keeps currencies honest, and makes transfers boring again.

That is the standard I would use for a real multi-currency net worth tracker.

If your spreadsheet already feels fragile, that is the signal

People often stay with spreadsheets for too long because the file still opens and the totals still calculate. That is not the same thing as the system still being healthy.

If you are already juggling several accounts, several currencies, and regular transfers, a proper spreadsheet alternative is not overkill. It is the thing that keeps your financial picture usable.

If you want a more trustworthy net worth tracker built on balances, transfers, and multi-currency reporting instead of fragile formulas, Expense Budget Tracker is a practical open source budget tracker worth trying.