How to Reset Your Budget After Overspending in 2026: Recover Without Starting Over

Overspent this month or blew past a few categories? Here is a practical 2026 budget reset: review the last 30 to 90 days, separate one-off misses from recurring leaks, cover overspending with real cash, resize categories, and rebuild next month without spreadsheet guilt.

One ugly week can make a whole budget look fake. Groceries ran high, dining out got sloppy, one annual bill landed at the worst moment, and now the month feels ruined. That is usually when people start searching how to reset your budget.

Not because they need a new budgeting personality, but because they need a way to recover from overspending without deleting the categories, starting a new spreadsheet, or pretending the month never happened.

That is the right instinct. A budget reset after overspending works better when it feels more like repair work and less like a dramatic breakup with your own numbers.

Overspending does not automatically mean the budget failed

This distinction matters more than people think. Sometimes you overspent because the plan was too optimistic. Sometimes the category was too vague. Sometimes real life hit all at once:

- travel for a family issue

- a harder month for groceries

- back-to-back social spending

- one forgotten annual renewal

- stress spending that made sense for about ten minutes

A useful financial reset after overspending starts by separating those cases. If you call all of them "bad discipline," you miss the actual fix. The goal is not to prove the month was acceptable. It is to figure out whether you had:

- a one-time miss

- a recurring leak

- a cash-flow problem

- a category problem

- a behavior problem that needs more friction

That is a much better starting point than budget shame.

Start with the last 30 to 90 days, not only the ugliest week

A lot of monthly budget reset attempts go sideways here. People look at one painful month in isolation, panic, and start rewriting half the system. Then next month turns out to have the same pressure points because the review window was too narrow.

I would use the last 30 to 90 days instead. Thirty days tells you what just happened. Ninety days tells you whether it keeps happening.

Pull in the real transaction history from every account that touched the month:

- checking

- savings if money got moved to rescue spending

- credit cards

- cash accounts if you use them often

- shared household accounts

If the data is scattered, import it first. This part is much easier when you are looking at actual transactions instead of trying to reconstruct the month from memory:

If you want the broader diagnostic workflow, How to Do a Spending Audit in 2026 goes deeper on the review side. The difference here is that a budget reset is not only asking where the money went. It is deciding how the next month should recover.

Separate one-off misses from recurring leaks

This is the point of the review. Not every over-budget category deserves the same reaction, so I would split the damage into two piles.

One-off misses

These are categories that blew up for a reason that is real, specific, and not likely to repeat next month:

- emergency travel

- a medical bill

- a larger gift month

- one annual renewal you forgot to stage earlier

- a temporary household purchase burst after moving or hosting people

One-off misses usually need funding, not a full category redesign.

Recurring leaks

These are categories that keep acting surprised by the same behavior:

- groceries over target three months in a row

- dining out looking "fine" until the third week every month

- subscriptions quietly stacking up

- household supplies hiding inside groceries

- transport running high whenever the schedule gets busy

Recurring leaks are where how to recover from overspending turns into category work.

If the same category keeps losing the same fight, the number is wrong, the category is wrong, or the rule is missing.

Cover overspending with real cash, not category theater

This is the least glamorous part, and it matters a lot. If you overspent, the next move is to show where the money actually came from, not where you wish it came from.

That means identifying one real source:

- money already sitting in checking

- money moved from a discretionary category that is genuinely being reduced

- money pulled from a sinking fund because the priority changed

- money taken from a general cash buffer

If none of that cash exists, the category was not covered. It was delayed.

This is where budgets turn into fiction. The budget grid says the month survived. The balances say something else. Then next month starts weaker than expected and the whole system feels unfair.

If your "buffer" is actually emergency money, be honest about that too. Raiding emergency cash for normal overspending is sometimes necessary, but it should look like an explicit tradeoff, not invisible cleanup:

I think this is the cleanest rule in a budget reset after overspending: overspending has to be covered by real cash, resized in the plan, or admitted as debt pressure.

Anything else is accounting makeup.

Resize the categories that keep breaking in the same place

This is where people overcorrect. They have one bad month and double half the budget. That usually creates a different problem: the new plan becomes too loose to trust.

A better reset is smaller and more specific.

Look for categories that need one of these fixes:

The category needs a bigger number

If groceries have been landing around 600 and the category is still set to 450, that is not discipline. That is fiction with a calendar.

The category needs a cleaner boundary

"Shopping" and "miscellaneous" are famous for absorbing everything nobody wants to classify honestly.

Split categories when the number does not lead to a decision. Household supplies, gifts, dining out, personal spending, and subscriptions often get cleaner fast once they stop hiding inside vague labels.

The category needs a better funding method

Some categories are not really "overspending" categories at all. They are variable or irregular categories being forced into a flat monthly number.

That is where this companion guide helps:

The point of a monthly budget reset is not to make every category stricter. It is to make the categories more honest.

If doom spending showed up, make the next month harder to wreck

This part deserves its own lane because doom spending recovery is not solved by renaming a category. When overspending came from stress, boredom, exhaustion, or one weird stretch of bad news, the budget problem is partly mechanical and partly behavioral.

I would not treat that like a morality tale. I would treat it like a friction problem.

A practical reset might mean:

- lowering the available discretionary amount for the next two weeks instead of the whole month

- moving extra cash out of the everyday spending account

- checking the category midweek instead of only at month-end

- separating "fun spending" from "I had a rough day spending"

- writing one explicit rule for purchases above a threshold

You do not need a dramatic no-spend challenge unless that is genuinely useful for you.

Most people do better with a budget that is a little harder to drift through casually and a lot easier to read in real time.

Rebuild next month before the first arrives

This is the part that makes the reset stick. Do not wait until the next month is already in motion.

Before it starts, decide five things:

- Which over-budget categories were one-time and can go back to normal.

- Which categories need a permanent number change.

- Which categories need clearer boundaries or a different name.

- Which transfers or cash movements need to happen before spending begins.

- Which one or two spending rules matter most for the next month.

That is enough. You do not need a grand reinvention after you overspent your budget. You need a version of next month that does not repeat the same failure mode immediately.

If the larger goal is building more breathing room so bad months stop cascading, read this next:

That article is about buffer-building. This one is about stabilizing the month right after the hit.

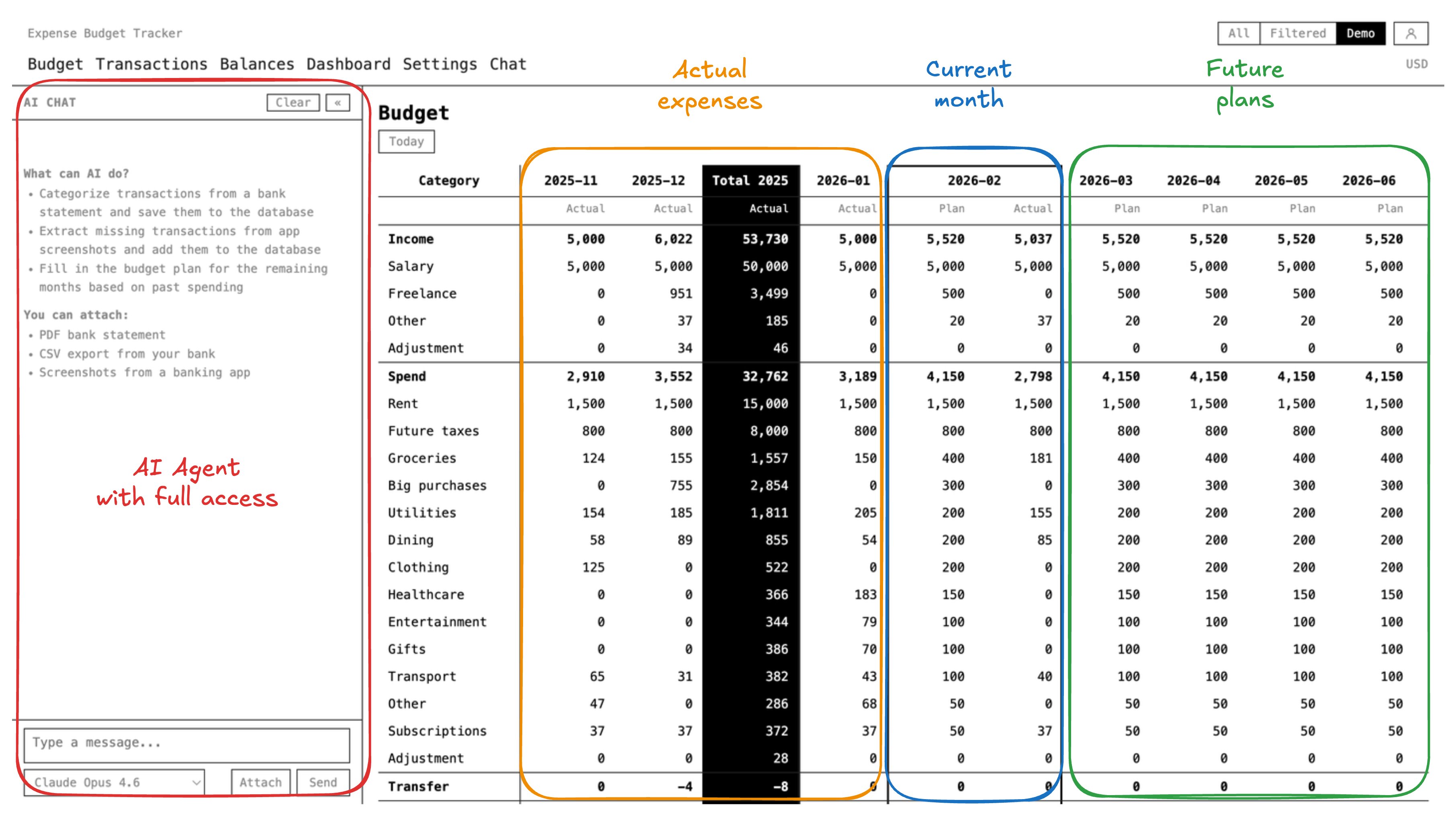

Where Expense Budget Tracker fits

Expense Budget Tracker is a strong fit for a budget reset workflow because the product already gives you the pieces that make recovery decisions easier to trust:

- a monthly budget grid with planned versus actual category visibility

- balances across accounts, so the budget and the cash position stay connected

- first-class transfers between your own accounts instead of fake spending

- dashboards that help you spot where the month actually drifted

- statement import workflows when the transaction history is spread across apps and files

- future-month planning, so the next month can be rebuilt before it starts

- an append-only audit trail for budget changes

- support for multiple accounts and shared workspaces when the money is not all living in one place

That combination matters because how to reset your budget is not mainly about writing a new list of numbers. It is about seeing:

- what changed

- what cash is actually available

- which categories are structurally wrong

- whether the next month is more realistic than the last one

If the system cannot show both category drift and balance reality, recovery stays fuzzy.

The useful rule

If you overspent your budget, do not start over.

Review the last 30 to 90 days, separate one-time misses from repeating leaks, cover the overspending with real cash, and resize the categories that keep lying.

Then build next month before it arrives.

That is the whole budget reset after overspending. Less drama, more repair, and a better chance that next month does not open with the same mess.